Are you an intraday trader cautious about trading super-fast with minimum latency?

Even before we answer your question – the more important question is – what’s the importance of latency in your trading.

- Importance of Latency in Trading

- Overall latency for Algo trading

- Latency for Manual Trading

- Latency in Server Based Execution for Exiting Trade (SLL, SLM, CO, BO)

- Use of Co-location

Related: How fast is order placement in APIBridge? What is the latency?

Importance of Latency in Trading

For automated trading, latency is key contributor to Slippage.

- Suppose you decide to buy Nifty when its trading at 9000. BUT by the time you punch order and get confirmation, you BuyPrice is 9010. In this case, slippage is 10 rs.

- Suppose you buy a stock at 100 and put SL at 99 (trigger price). Your SL gets triggered but you get SellPrice of 98.50. In this case, your slippage is 0.50.

- If you make 5 trades per day by 10 orders, and slippage per order is 0.2%, then you are losing 2% per day!!!

- If you make 2% per day, in a year you can grow your money 100 time!

Retail traders make money because of their overall trading system, and not just speed of execution. APIBridge helps you in all components of system trading. Remember: “The whole is greater than the sum of its parts.”

- Trading Logic or Conditions for Buy-Sell decisions (technical or quantitative)

- Risk Management (stop loss, target, daily loss, volatility adjustment etc.)

- Order/Slippage Management (order types, product types, margin management, managing open orders etc.)

- Position Management (scale-in and scale-out)

- Portfolio Management (trading in multiple symbols, multiple strategies, multiple market segments)

You see from the list, speed of order placement has little importance in system trading.

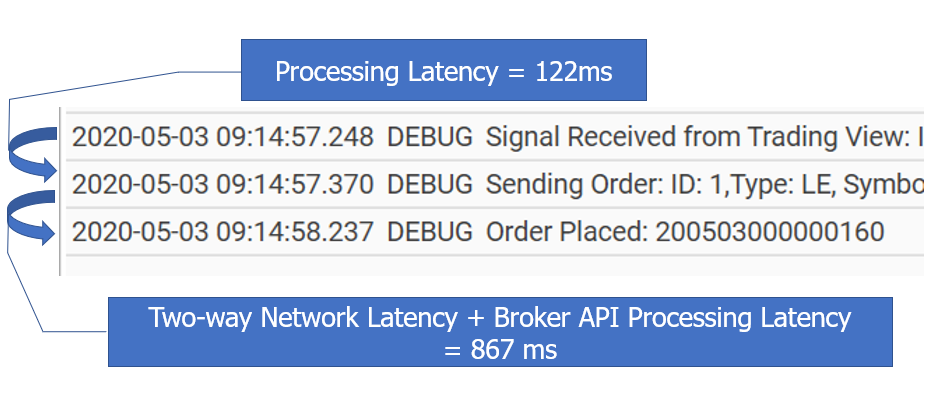

Latency for overall algo trading

The latency for overall algo trading is 1-2 seconds, under normal use case.

- Real-time price update (last tick) in charting platform (Propagation Latency)

- Time taken by script (such as AFL/VB) to do calculations and generate trigger (Processing Latency)

- Time taken for passing trigger from charting platform to APIBridge (Processing Latency)

- Duration took by APIBridge to process an order (Processing Latency)

- Time taken by your internet to send the order to broker (Propagation Latency)

- Time taken by Broker to process the order (Processing Latency)

- Duration took by your internet to send Order Confirmation (with Order Number) to APIBridge (Propagation Latency)

- Time taken by APIBridge to process Order Number and Send Request for Order Status to Broker

- Time taken by your internet to carry this request from APIBridge to Broker (Propagation Latency)

- Duration taken by Broker to process the Order Status (Processing Latency)

- Time taken by your internet to carry Order Status from Broker to APIBridge (Propagation Latency)

- Time taken by APIBridge to update the order status (such as pending or filled) (Processing Latency)

Related: How fast is order placement in APIBridge? What is the latency?

Latency for Manual Trading

The latency for overall manual trading is 5 minutes, under normal use case.

- Time is taken to analyze data and decide whether to buy or sell using personal discretion. This takes several minutes for even the fastest intraday traders.

- Trade Entry: Time is taken to fill up order parameters, confirm and submit an order; and then modify the order if required ~ 30 seconds

- Trade Exit under the similar process of Trade Entry ~ 30 seconds

Latency in Server Based Execution for Exiting Trade (SLL, SLM, CO, BO)

In many conditions, such as square-off on profit target or stop-loss, the trade exit may be executed by the broker’s server. This can be extremely helpful because such execution saves money from slippage. As an example, say you have set up SL of 8000 in your charting platform. It may take 1-2 seconds of latency to complete the trade, and during this time the market may have already moved by 3-4 points. If the lot size is 75, this will translate to losing Rs. 225 per trade. On the other hand, say if the broker’s server executes a sell order when the bid drops to 8000, it may just be able to exit your trade at the desired price. Hence execution at the side of the broker server can drastically reduce latency as well as slippage.

Use of Co-location

Colocation is the practice of running your strategy at the exchange’s server to minimize distance. Hence it minimizes latency with greater bandwidth and a host of other professional advantages.

The NSE server rack is available at an annual cost starting at Rs. 6.5 lacs. The detailed specs can be found here: https://www.nseindia.com/membership/content/connectivity.htm

HFT programs try to exploit short-term alpha which lasts in prices from nanoseconds to few milliseconds. The slightest latency for HFT is the difference between profit and loss.

HFT was a fad in 2008 in India. Right now, in 2020, the number of HFT Desks is down to almost 5% compared to the 2008 level. HFT is a race of technology and infrastructure, in which only the biggest players survived. They cannibalized other HFT players and hence the downfall in a total number of HFT players.

Recent Discussion